Care Credit Consumer Reviews

By sandra812 -

By sandra812 - I just got off the phone with a CareCredit customer service rep, and I was hoping they would actually have me complete the survey they promised at the end of our call because I would have been happy to air my grievance there. But, no surprise, there was no survey after our call, so I'll grieve here instead.

A previous reviewer talked about the rudeness of the customer service reps--100% agreement! First I was given a woman with such a thick accent that I couldn't understand a word she said. Wanting to be kind, I told her that her accent was beautiful, but that my hearing wasn't great and I was having trouble understanding her, and asked if I could speak with someone else. She sent me to a whole different department (merchant services) that couldn't help me at all, and they sent me back to customer service. This time. I got a rude lady (no accent). She had zero skill in soothing a customer's ruffled feathers--why are people like this given customer service jobs?

I complained that even though I faithfully make my monthly payment on time, and pay my full balances within the demanded time, I have been charged interest and a fee this year on my balance. She explained (in a tone that sounded like, "You idiot, you should know this") that a portion of my bill had been "non-promotional"--she kept repeating this phrase as though I should know exactly what that meant. I finally told her I didn't know what she meant by "non-promotional", and only then did she go out of her way to explain that if your bill is under $200, you get charged interest until that portion is paid off!

I also told her that the chat feature which their site claims to have was nowhere in sight on my computer. She said to go to Internet Explorer instead of Google Chrome and it would most likely be there. I tried that and, again, there was no chat link to be found. She said, "Well, I'm on that page and I see it on mine"--in that same condescending tone, as though she was certain I was looking straight at that chat button but was just too stupid to see it. Never did resolve that one--the chat feature simply wasn't there. Last thing I needed was a copy of an old statement which wouldn't print at the time I tried to print it (Their site is tweaky sometimes and won't cough up what you need).

She asked if I wanted a paper statement sent. Suspecting hidden charges on everything with this company, I asked if there was a charge for that, and she informed me in her "what idiot wouldn't know there was a charge?" tone that it would cost me $4. In surprise, I mused, "A $4 charge..." Her cold response: "Yep." Very short with me, very uncharming, terrible representative of the company. I told her I would be glad to respond to their promised survey--but that never came. I had been telling others about CareCredit and right now have two friends who were going to look into getting it for their vet needs. I will advise them otherwise.

Replies

Replies

By Nermy -

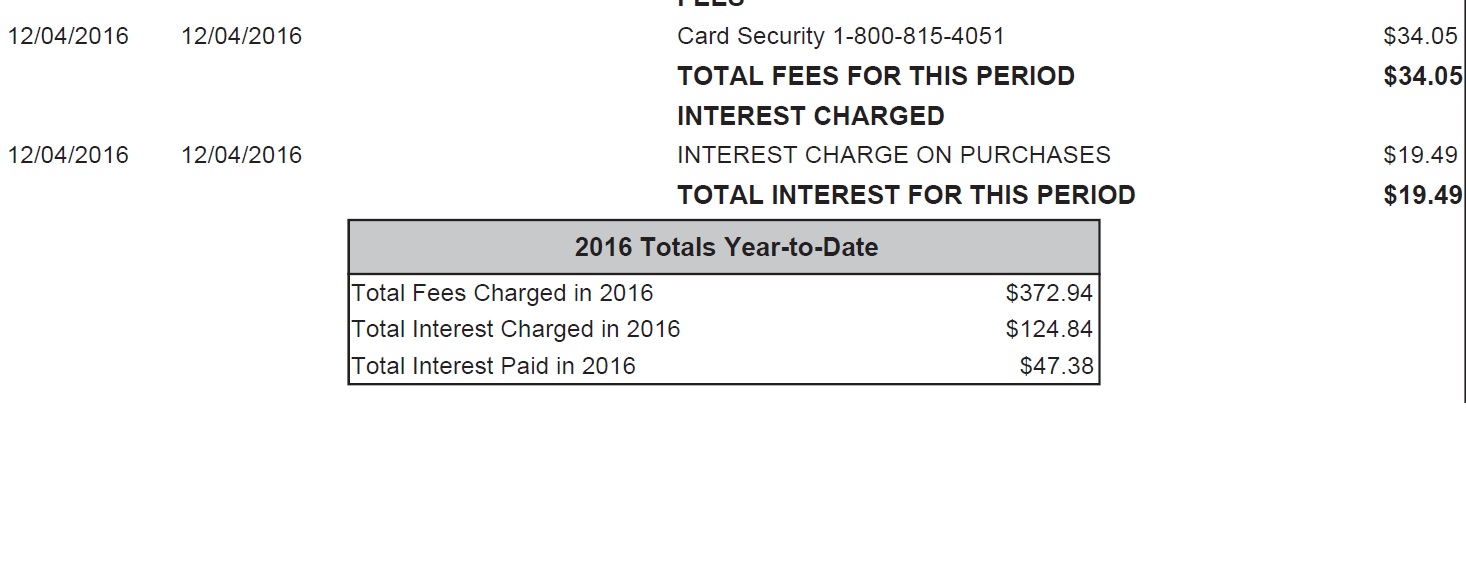

By Nermy - ANCHORAGE, ALASKA -- They say they don't charge interest. But they actually do. It is charged in the first few months of using it and you start paying on it right away. On a $1,500 line, I had a 12 month promotional period of "No interest charged" if paid within 12 months. Total lies! They started charging interest immediately plus they charge service fees! Within those 8 months I had to pay $370 something in service fees and more than $125 in interest... on an interest free loan... wtf. Total crap company. I would never recommend them to anyone and I am actually going to as many reviews sites as possible in an effort to help people make the RIGHT choice and FORGET CareCredit. Total scammers!

Replies

By CareCredit Is A Rip-Off -

Replies

By CareCredit Is A Rip-Off - ORLANDO, CALIFORNIA -- The dentist clinic suggested and help me file for financing with CareCredit on April 2017 and promised a no interest until December 2018 for a $6,000 loan, it is June 2018 and I've been making my monthly payments on time yet all of a sudden I see 3 interest's charges totaling $1,700 interest charge! How is that possible that they charge so much and also before the time they promised?

Replies

By Lovelette - BROOKLYN, NEW YORK -- Received CareCredit approval on the 12/29/2016 for a tested glasses. I didn't want to run my credit for that but at the doctor's office they told me the one my personal insurance offer won't help me, so they offer to get me another through CareCredit. I gave in they ran my credit. I was approved on the spot for $1500 CareCredit. The lady at the doctor's office said, "You received a discount," so I would only pay $950. CareCredit reported the purchase to my credit on the 12/ 31/2016 with a zero balance.

I received an alert on the 1/17/2017 that my account was flagged and closed with a balance of 950. The craziest part of that is the glasses wasn't ready for me to pick up until the 1/17/2017. I went back to the doctor's office, inform them about what took place with CareCredit, and also told them when they wanted to give the product to me that I don't need it anymore.

I called CareCredit and spoke to Customer Care. They told me that they're sending me a mail to say what happened. CareCredit accounts manager said he can't give me the details of why they approve me for credit so fast and closed the account so fast without as much as a call to me. I was told by him they're sending me a letter to state the reason. I called Experian credit tracker and reported it to them so they immediately put it into dispute right away. Something is definitely not right here. This to me is very shady. I wouldn't recommend CareCredit to anyone.

Replies

By TK - ORLANDO, FLORIDA -- After no contact for a year, these lowlifes start charging me 29% interest, I find out and want to pay off the $300 I owe (I have been on automatic payment for 11 months). Four days before my call they tacked on almost $400 interest for the past year. I want to pay the whole thing off, and that is now almost $800.

It also took over an hour on hold before I could talk to anyone in a managerial capacity as they only have one line from customer service to management and it is always busy. These people did not notify me of anything, no emails, no snail mail, nothing, they tack on all this interest without an opportunity to pay off the balance. This company should be investigated and put out of business.

Replies

By junk - DRAPER, UTAH -- This is the most USELESS operation I think I have ever experienced. I applied for this credit with a credit score of 720 in which I think is very good for this day and age. And it asked for the amount that I needed to borrow which was $3400. After I hit the go link, I was automatically approved. All good. But it only gave me a $800 credit. Now my credit is in the good range and I told it the amount that I needed but it chopped 30 points off my credit which puts me into the average in credit score and all for nothing. The card is useless to me and now my credit score is butchered.

So I call to cancel this useless card. Now they say that it could affect my credit score as a bad creditor and butcher yet more points. This is by far the worst line of credit for medical there is and definitely a disaster to your credit. So if you have a miracle doctor that still only charges a few bucks for visits or a dentist that's under $1000 that you can use then maybe this is good for you. BUT if you have a perfect credit then you won't need these crooks. Stay away from these crooks.

Replies

By Steve - This is an open letter to anyone interested in open a Care Credit account. Simply do not do it. My fiancée had to get some dental work done, which was not covered by insurance at the time. So the dentist offered her a Care Credit card with should be paid in full over the course of a 12 month period. Well what they do not tell you is how ** terrible their services really are; after “paying” online for the first 3 months through their website; it turns out none of those payments ever went through; so she incurred $125 in late payment charges for the first 3 months, taking her original payment from $504 to $650.

Over the course of the next 4 months from January until now she has paid $100 a month for the last 4 months. Her bill in January was $554. For Feb was $454. For Mar was $254 and paid. It was down to $154 and now this month it's back to its original cost of $504.

These people are shady and need to be investigated with a lawsuit of fair practices and debt collection. They literally add on a $10 or $11 charge every time you call them to make a payment since their web service sucks so bad. On top of that the “No interest charge” is a ** lie since they will charge you interest on everything that is not the original payment. "Oh you have a late payment." HAHAHA INTEREST. "Oh you called us about your account." HAHAHAHA INTEREST. We have sent in our bank statements to prove that we have paid the last 4 months without being late, and they “HAVE NOT RECEIVED THEM”.

Replies

By Care Credit Victim - FLORIDA -- For convenience I used Care Credit for a dentistry bill. All went fine with my automatic monthly payment through my bank. No interest, no late fees. After it was paid I again used it for husband's new glasses. I set up a similar payment schedule for the glasses, same date with different monthly amount, of course. On a fixed income, automatic payments are a must for me.

I was unaware that, unlike normal credit cards, the payment date did not remain the same & had changed to 4 days before I had scheduled the automatic payments. I received no late payment notices, but over a 6 month period I was charged $158 in late fees! The initial statement for the glasses included a $55 payment that was not even due until the next month!!! Yet they are saying that the early $55 payment does not count as payment for the next month. That amount was over twice the minimum payment amount, but all that gets me is a "Thank you".

Yes, I should have looked carefully at the statements that were emailed to me, but I was thinking "Credit card - same pay date - all set up with my bank" & just skimmed over the statements. I did not check the statements until I saw that their balance was much different than mine. I called them & was able to have the outstanding balance waived & set to zero, but that did not cover all of the late charges. They will not refund me nearly $70 in overpayments.

Replies

By S. - RACINE, WISCONSIN -- I applied and was approved. I was told wait somewhere around 10 days for my card. (Can't remember the exact amount now) I never received it. I called and was rudely told to wait longer. I ended up cancelling the card not knowing Care Credit reported a lost or stolen card to the credit bureaus, dropping my score 13 points. Of course my old card comes the next day, later than supposed to. But now I can't do anything with it because it's already been cancelled. Now I have to wait for the new one. I called and complained, and it was supposed to be corrected. Never was. Then they reported an account closed and it dropped another 12 points! I called and complained again. They reassured me that I would get my points back once it was reported an account was opened again. I had them dispute this with the credit bureaus and I lost another 6 points due to a "remark added/consumer dispute". If you are like me and closely monitor your credit report because you have worked harder than hell to build your credit; finally recached the 700s, and lost 31 points! Be careful with this one!

Replies

By You have been warned - DALLAS, TEXAS -- A fellow employee informed me they were being charged a credit card security fee. I reviewed my billing and found I was being charged for the same line item. After trying to pay them off for a few years, this unsolicited fee added up to over $4,000.00. I am happy to say they will be giving me a credit for this charge. Watch all of your bills from this company if you do not want to go through my pain. Soon this company will be out of my life and have gained another person that will warn others of doing business with them.

Replies