United Healthcare Consumer Reviews

By ChyAnne -

By ChyAnne - SALT LAKE CITY, UTAH -- I am so surprised to see bad reviews! I had this insurance in 2014 through my husband's employer and ended up needing a hysterectomy in December 2014. My husband's employer had already decided to switch insurance companies in Jan 2015, so I was in a time crunch.

I went on Dec 8th for pre-op evaluation, and my surgery was scheduled for Dec 18th. Unfortunately I found on from the hospital on Dec 17th that the insurance had not yet approved the surgery, because pre-approval had just been submitted by the doctor's office that morning, the day before my surgery.

I called the insurance company in tears to get this surgery done, as I was in pain, and I was told she would do everything possible to get it taken care of. I also stupidly disclosed that we would be changing insurance companies in a couple weeks and I didn't know what the coverage would be and I had already met my out-of-pocket annual maximum - a perfect reason for them to delay approval to not have to cover.

Imagine my surprise to get a call at almost 8:30 pm (well after closing time) to tell me it was all taken care of, I could have my surgery the next morning. Surgery was done, bills were paid, no problems. A few months later the anesthesiologist was billing me, saying my insurance didn't pay them. I looked at the EOBs, which said I owed them $0 due to network discounts, so I called and told the provider this. They said OK, no problem.

A few months later (after my coverage ended) I got a call from the anesthesiologist again saying I owe, and that they are not in network with my insurance. I called UMR and they got on 3-way call with me and the provider and told them they are in network. The anesthesiologist office said "I don't care. We are billing it."

True to their word they sent me to a collection agency. I told them what happened (Note this was almost a year later, long after coverage was terminated with this plan). I called UMR and they send documentation to the provider showing their in-network status with a copy of the contract. The collection agency continued to call and I continued to explain to them and they told me to call the provider, which I did, and they said they would look into it, which they didn't.

Fast forward to today, March 2016, 15 months after my procedure and the termination of my UMR plan - the collection agency said I need to send EOBs to show I don't owe the balance by the end of the day or my credit is going to take the hit. I called UMR with no ID, no active plan, and no benefit to them whatsoever and spoke with Natalie, a super sweet woman who looked up all EOBs for anesthesia (as they did not bill under their business name, but under a provider whose name the provider couldn't tell me), and she faxed the EOB immediately and waited on the phone to make sure I got it. I faxed it to the collection agency; game over - I win.

UMR reps were always understanding, helpful, accommodating and expedient. I know they say people are more likely to leave a bad review than a good one, but I believe this company definitely deserves credit for the assistance they provided me, and continue to provide long after my coverage was ended. I would recommend them to anyone looking for good customer service.

Replies

Replies

By Bree -

By Bree - MARKET PLACE, FLORIDA -- WORST, WORST, WORST experience ever! Here's my experience... (Personal information has been changed for my privacy). 2012 - Signed up for individual insurance for "Suzy " (female) with United Healthcare Golden Rule. March 2015 - Signed up for individual insurance for "Suzy " (female) with United Healthcare MarketPlace. - March 2015 - Marketplace plan was started, and month 1 paid. ID **. March 31, 2015 - Marketplace plan was terminated without communication to either Suzy or Stewart. March 2015 - No payment made to United Healthcare Golden Rule.

May 2015 - Suzy realized she never received an insurance card from the MarketPlace and could not log in to their website. May 2015 - Stewart (Insurance Agent) and I ("Suzy Anne " (female)) called United Healthcare MarketPlace regarding plan established in March. Response was that the plan never went through, and a new application was filled out over the phone. New application used the wrong name (Anne as the first name, as the surname, no mention of Suzy) and indicated insured was a male. Suzy paid $713.72 to cover the balance from April and May. ID **.

May 2015 - United Healthcare mailed Suzy 2 letters regarding outstanding balance of $38.62 and a period of 10 days to pay the balance. Suzy was out of the country and did not receive either letter. No communication was made via email or telephone to either Suzy or Stewart regarding payment issue or coverage termination. July 20, 2015 - Physician office calls Suzy regarding insurance had been terminated. ID **.

July 20, 2015 - Suzy and Stewart call United Healthcare, call was disconnected. Suzy called United Healthcare back and spoke with a customer service. She was advised her insurance had been terminated for lack of payment. Bank statements indicate a check for $224.11 was mailed to United Healthcare each month, yet according to the United Healthcare representative, none of those payments were attributed to Suzy 's account. According to the bank, they were all cashed. Suzy was advised to send an email and explain the situation. An email was sent (to uhcexchange@uhc.com) and Stewart was carbon copied.

July 21, 2015 - Email from United Healthcare was received by Stewart that read "We will make the exception to reinstate without lapse with the additional $38.62 and the June payment of $262.73 for a total of $301.35. The insured can call and pay with a cc payment today or they can send a payment to us to be received by the close of business on 7/23/15, after that date we will not be able to reinstate without lapse."

July 21, 2015 - Suzy called United Healthcare, paid $301.35 and was advised her account would be reinstated. This reinstated her Golden Rule account from 2012 (ID **), not her most recent MarketPlace account. Suzy was transferred to the MarketPlace, however after speaking with someone and waiting on hold for more than 30 minutes, the call was disconnected. Prior to being disconnected, Suzy was advised that she paid $713.72 in May, and her account had been terminated at the end of May.

July 22, 2015 - Suzy called United Healthcare Marketplace to get reinstated. She was advised that her account (ID **) had been terminated in March. The representative advised a new application would need to be filled out. They found Suzy's name was written as Anne and she was identified as a Male. The call was disconnected before the application could be completed.

July 22, 2015 - Suzy called United Healthcare Marketplace to get reinstated. She was informed that there was nothing she could do as her insurance had been terminated. Call transferred to Tier 2, who sent a request to United Healthcare Case Management to reinstate insured. Suzy was advised the process could take 1 - 2 months. No record of May's payment or Golden Rule account was found. July 22, 2015 - Suzy called United Healthcare Golden Rule to confirm insurance coverage secured the day before (July 21, 2015). Her ID (**) could not be found in the system.

July 24, 2015 - Suzy and Stewart called United Healthcare MarketPlace to discuss coverage. Their system did not reflect calls from earlier in the week, nor did it correct the name "Suzy Anne" and "Anne." Service representative Lance advised call would be elevated to someone that could problem solve and worked on odd situations; United Healthcare MarketPlace should be in touch with Suzy in 5 - 7 business days with a resolution.

July 28, 2015 - Case management called and left a voice mail. Name (first name only) was not understandable. Did not leave a case number. Call was to informed me they had my case and would be working on it. July 27, 2015 at 6:20pm. Called number left on the voice mail (877-887-0441), no notes regarding case management, case manager or case number. Called number that called me (**), call was disconnected.

July 31, 2015 - The MarketPlace called to inform me my application has been updated. Marketplace has updated my application. Sent the application and a request for reinstatement to the UHC. Have to work with UHC to get reinstated. Has no information about payments, old policy ID number. At this point I have to work with the plan (aka UHC). Name and sex have been corrected. No idea who at UHC I need to talk with. Advised her that my policy got messed up because the Golden Rule and MarketPlace systems didn't catch the error in my application.

She asked why not, and I said it was because the systems don't communicate and neither do the people. She said I would need to work with the insurance plan. I asked who that was and she said the plan. After asking for clarification again, she said it was UHC. I asked which department at UHC I would need to talk with since if I called then and said, I need to talk with the Plan, they would think I sprouted a second head. She said she didn't know, she wasn't part of their company and doesn't know their departments. She doesn't communicate with them.

July 31, 2015 - United Healthcare called. Received a file from the MarketPlace on 7/15 showing termination should have been 3/31. As of today, UHC has not received anything from the Marketplace. If the Marketplace sent something, it will take about 30 days to process. July 31, 2015 - A letter from Golden Rule and check came in the mail today. The letter states that I am paid through July 31, 2015 and in fact overpaid by $224.11. The check is for $224.11.

Here are the issues: This payment was made through the website that we set up access to while on the phone with the Marketplace in May 2015. This payment was applied to my old Golden Rule account from 2012. I was dropped from the Golden Rule account in May for non-payment. The Marketplace won't show record of this payment. I also received a letter from the Marketplace that says I am eligible to re-enroll in January. This is the first communication I have received from the Marketplace.

March 2015 through current - Suzy never received any communication, a new card or an invoice from United Healthcare Marketplace. March 2015 through recent - United Healthcare Golden Rule has been charging Suzy for an old plan, collecting payments and not attributing them to her account.

Sent them: Bank payments for United Healthcare Golden Rule. May payment for United Healthcare MarketPlace

American Express payment for $301.35 for United Healthcare Golden Rule, made July 21, 2015. Total paid to United Healthcare 2015. Jan: $224.11. Feb: $224.11. March:. April: $224.11. May: $224.11 and $713.72. June: $224.11. July: $224.11 and $301.35. Total: $2,359.73. Marketplace premium: $356.56. Owed to United Healthcare for = $-35.85.

Replies

By OL - NEW YORK, NEW YORK -- I am currently covered under my husband's employment, health plan, and I am also retired and have Medicare part “A” only. United Healthcare refuses to pay for my doctor bills because they say I am covered through any other plan, when, in fact, I only have Part “A” on my Medicare plan. I tried appealing, and I tried calling them to tell them that I only have Part “A'” not part “B" but they don't care.

Replies

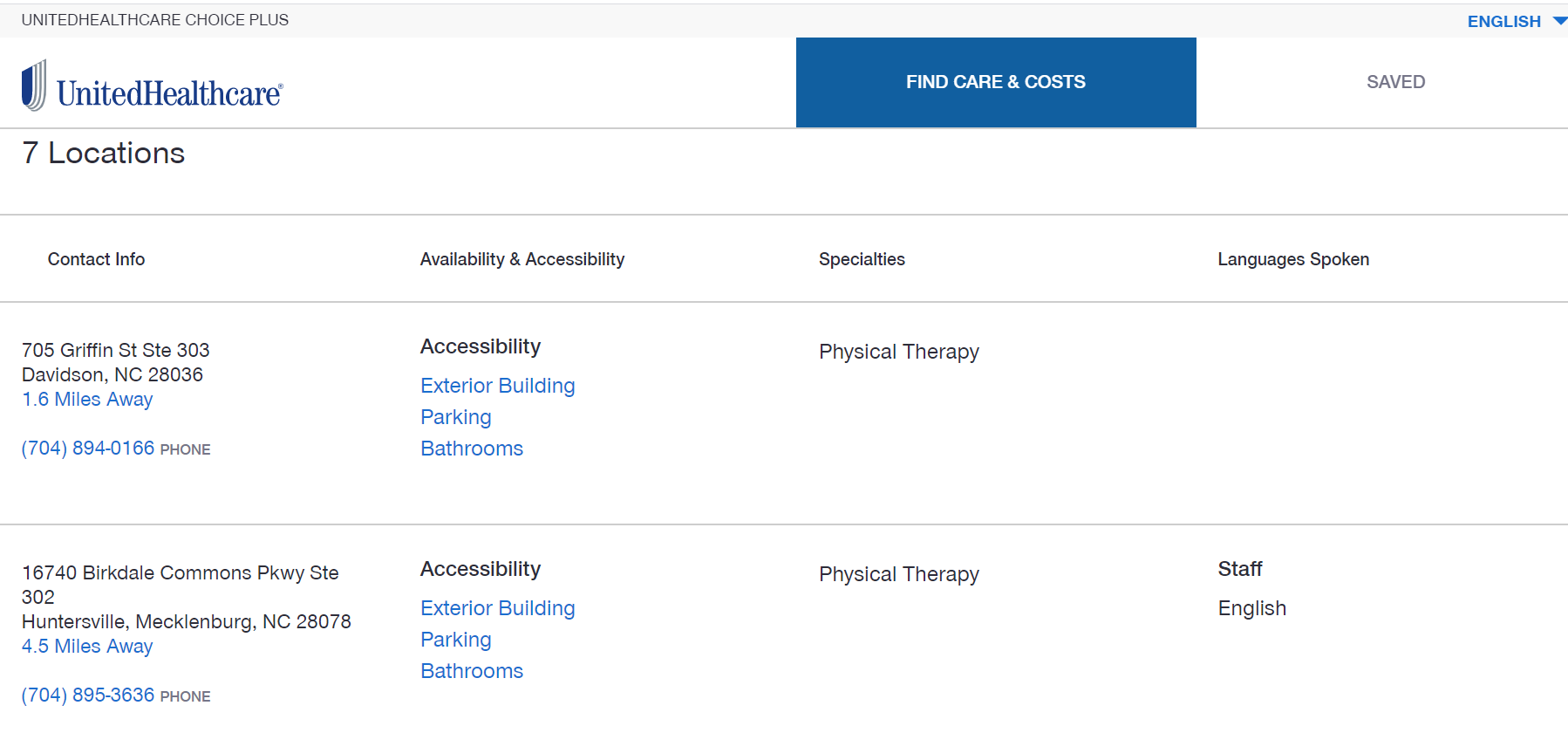

By RB52 - DAVIDSON, NORTH CAROLINA -- I needed to get Physical Therapy done and I called a Facility close to me that confirmed that they are in network for my insurance. I also checked and confirmed that they were in network for UMR/UnitedHealthcare website. In addition, I also called Grand Rounds (3rd Party that helps with insurance questions for my employer) and they also confirmed that this facility was in network. Once the claim was filed they told me that I went to an out of network provider. I checked online and my facility still shows as in network.

If they are out of network then UMR/UNC is committing a fraud by telling its customers to go to an in network provider and then processing the claim as an out of network provider. Other than this situation, I've had some sort of an issue with every claim that was filed. United HealthCare used to be good but when UMR took over I've had all these issues and if my employer gives me a choice I would never sign up for them again. I'll be definitely giving this feedback to my employer as well and hope that they can offer the employees better options in the future. Attached is a screenshot showing that my facility is in network.

Replies

By Eric -

Replies

By Eric - PEORIA, ARIZONA -- Hurt my back 5 weeks ago. Got the MRI and results last week. Have a fractured vertebrae. Have not been able to work for the last month because it's so painful. My doctor's office just told me it would take 3 weeks for pre authorization to have a kyphoplasty to correct it. If I lose my job or my ability to use my legs due to this hold up, I will sue the hell out of UHC, be assured of that.

Replies

By Mike - My daughter has seizures, and the original medicine she was prescribed (which UHC covered) caused bad side effects. She would turn into a different person for the first couple hours after taking her medicine. She was almost manic! As the medicine wore off each day she became depressed and mopey. Her school work was also suffering, and the teachers were asking us if there was a problem. She had previously been a good student and all the teachers loved having her in the class. This was at a low dose of the medicine, as the doctors were ramping her up to the normal dose for a child her size.

After discussing with the neurologist, he then prescribed a new medicine. The new medicine was the same as the old, except it was time release. With the new medicine she has gone back to her old self, and doesn't experience wild mood swings. Unfortunately, UHC will not cover the time release medicine. Because the time release medicine contains the same ingredients as the cheaper first medicine, they will only cover that medicine. We have appealed, with doctors and teachers writing letters to describe the side effects of the first medicine. None of this matters to UHC.

We will continue to pay the $650/month for the time release version. We are lucky enough to be able to afford this. However, I feel for those in the same situation who are being denied and can't afford it. We probably would take her off the medicine completely and risk further seizures if it meant going back to the first medicine. Prior to this happening, UHC denied my cholesterol medication. This medication had previously been allowed by Humana before my company switched providers. My specialist told me I was better taking an over the counter version instead of the medication UHC would cover.

However, he recommended I continue to take the non allowed medication. I did continue to take this medication until we had the issue with my daughter not being covered. At that point paying the monthly amounts for both was not an option, so I have discontinued the cholesterol medication. UHC has a well-earned reputation for not covering medical necessities. They offer lower premiums to companies, and then make up the profits by not covering items the doctors feel are important.

Replies

By Laurakosb - PITTSBORO, NORTH CAROLINA -- This letter will be copied and placed on the webpages of all companies. My story begins almost a year ago. My husband (a Duke Internal Medicine patient) was scheduled for a follow-up colonoscopy after having multiple polyps found the year before. In the course of the year, my insurance changed and we secured Marketplace insurance with United Health Care. This was premium insurance, very expensive monthly premiums and a $250.00 deductible.

The provider's office did a referral, and here is where the water goes murky. Duke, at the time did not take the type of UNC insurance (compass platinum), so an appointment was made via the providers office with UNC healthcare. My husband called UHC prior to the visit to make sure the paperwork was in order and was told "the procedure was a covered 100%". He had the procedure, and received a bill. Part of the bill was covered but 2900.00 was not. Upon investigation per UNC, the referral was for a screening, not diagnostic and needed a new number.

The provider office said the referral did not need a number and would look into it. UHC said the referral was not correct as well. After multiple phone calls with all three groups and a lot of finger-pointing between companies, the bill was turned over to collections, and UNC will not return phone calls.

A customer service representative from Duke has also looked into the situation and told us today, everyone is blaming someone else. Here is the sad thing, all these companies advertise "patients first, patient centered care" etc. The patient should not be responsible for making sure referrals have a correct number, should not be responsible for making sure codes are correct. He did due diligence to make sure prior to the procedure that it was covered.

The final disservice and disrespect to the patient is making them jump through hoops to find out no one is accountable but him. $2900.00 may not be a lot to some, but it is a lot to us. Add the monthly expense of the insurance premiums, for what should be covered and this is shameful.

Replies

By jwb - MINNESOTA -- I have received yet another denial letter from UHC in response to my BBB complaint. They basically rehashed their denial stating it was just an "estimate" and referred me to the "Why Costs May Vary" section. I would understand if they gave me a different amount for my Out of Pocket expense (say $100 & that in actuality it turned out to be $150), but they told me it was 100% covered for a 57 yr. old & that my Out of Pocket amount would be $0.

Had they told me it was only a covered benefit for adults 60 yrs. of age or older or that it would have been 100% covered if I went to the pharmacy to get the shingles vaccine, I would have waited the 3 yrs. (now 2 yrs.) to get the vaccine or gone to my pharmacy where it would have truly been 100% been covered. They gave me the wrong information & will not accept responsibility for their mistake. I was never given the external review from someone outside of UHC even though I had asked for an external review 4 times.

They have basically given me the runaround for 16 months in the hopes that I will give up. They hide behind jargon and twist it to their advantage. Any average person being told "Good Job on Preventive Care" & that the shingles vaccine is 100% covered with $0 Out of Pocket expense would assume that it is a covered benefit. Why would you think otherwise? They are exhibiting "bad faith" all around.

After all this, wouldn't it be a sign of integrity and responsibility just to pay the $210 instead of spending probably hundreds of man hours and dollars to continue to deny the claim. Every correspondence ends with "Your satisfaction is important to us." That is so very far from the truth. If that was true, they would have paid this claim long ago & not ruin my credit by having the claim go to a collection agency.

Replies

By Kim - TENNESSEE -- My father needed to have a CT scan per his doctor to make sure that his cancer (has been cancer free since 2000) had not come back. His claim was denied by United Healthcare. The reason stated was "You have cancer in your nose and throat area. You have neck pain. You have a sore throat and pain in the roof of your mouth. Your provider suspects spread of "cancer" to your brain. Your provider asked for a CT scan of your head/brain with and without a dye called contrast."

The letter goes on to explain what a CT scan is and what a MRI is and then states that "cannot be done for medical reasons and you have a brain function problem such as mental confusion, change in vision, slurred speech or a new severe headache."

My father receives this notification and is devastated!!! First of all, he went the doctor with throat and pain in the roof of his mouth. He NEVER complained of headaches, mental confusion, change in vision or slurred speech. He contacted his doctor and the head nurse called back and apologized over and over again since the information that was sent to him was a LIE!!! She confirmed that no one in the doctor's office provided that information to United Healthcare. It appears that someone that works at United Healthcare falsely added this information/LIES to his records so that the medical services requested would be denied.

I am sure this is not the first time that this has happened to customers of United Healthcare. Please do not use United Healthcare for your medical needs because they falsify medical records so they do not have to approved medical services or items. How many others has this happened to? Who can help with this type of fraud?

Replies

By cloudydays9778152 - SALT LAKE CITY, UTAH -- United Healthcare mailed me five provider appeal requests I never made. I got four in November 2014 and the last one dated December 5, 2014. First one gave the name of a company and said I made a complaint against this place and said they sent a decision explanation and since it was a duplicate, I couldn't appeal it. What complaint and what duplicate complaint? I've never made one. I faxed UHC in November 2014 and informed them that I did not make a report and for them to correct it. Ignoring tactics they use. They sent me four more of the same.

They were dated November 4, 7, 17 and 25, 2014. UHC indicated they put them in my patient ID files. The last one was December 4, 2014 and dated with an individual's name as provider appeal request I never made. I faxed provider complaint on a horrible P.T. records content that UHC had paid for and last phone contact about that was October 27, 2014. Last fax regarding that was November 2, 2014. I never heard back on the issue about P.T. session.

I got harassed by UHC with nut job fake reports instead, gee I wonder why. Also November 3rd and 4th, I got two phone messages to call UHC about another made up nonexistent report. Saw bad scene, I was done with UHC. No more phone contact and I looked for another insurance. I would have had to have made a report and received a letter back on an appealed decision in a specific time frame long before the P.OT.. complaint to have even exist, which it was not.

They have NO phone connection or faxes or letters on fake reports. I got 2 answer machine calls on December 5 and 8, 2014, from service coordinator UHC, phony, prank sounding message telling me to call her about my requesting multiple therapy times. I never did! I stopped all calls. October 27, 2014 was the last and only sent a few faxes November 2014 for UHC to take reports I did not make out of my files. And I did not of course, pursue initial complaint.

I left UHC in December 2014. They also apparently sent me to physical therapy two other times , pulling a stunt of having my significant medical condition completely left out and had my other med files hoaxed with as medical conditions magically deleted. My only opinion is all of the above. I have all of my medical records however. I've been trying to get all the fake files out and straighten the records out through other places, but not able to yet. I have not gotten five fake file reports I never even made. I do not have anything to do with UHC!

Replies