AAA Consumer Reviews

By Hurt -

By Hurt - MONTGOMERY, ALABAMA -- I have been with AAA towing company for 40 years. I was coming back in town and my car alternator quit. I needed a tow and they said I was 3 or 4 days it is expired. AAA said they would send a tow truck anyway. The truck driver was very nice. My house was not far but when he dropped off my car he said it would be 300.00 dollars. I have been paying AAA insurance in the amount of nearly $90 a month for all these years. I quit AAA company, this company that would not go back a few days and help during these bad times. I got insurance from Allstate and they are superior to AAA towing company.

Replies

Replies

By AzGal -

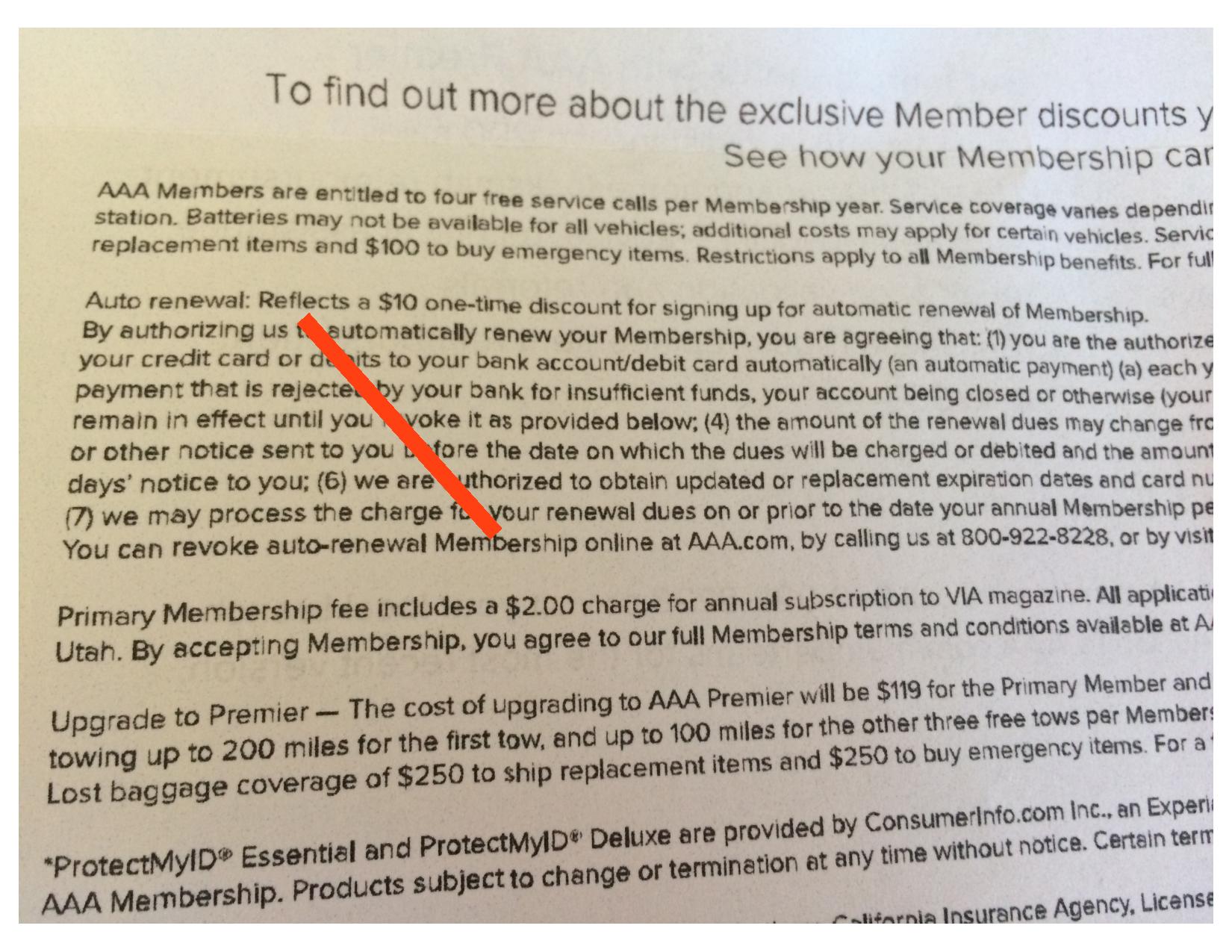

By AzGal - ARIZONA -- I have been a member since 1987 and am pleased with their road service. However, I now find out that I am being forced to pay $2 every year for a subscription to their magazine. I do not read it and it goes right into the recycle bin when I get it. If someone wants it then I am sure they would be happy to pay the $2. But why should people who do not want the magazine be forced to pay for it?

I contacted Customer Service at 800-922-8228 and was told that that was just the way their "system" is and that perhaps if more people complained about it they would change their "system." Their "system" in this regard is a bad one. If they want to use $2 of my membership dues for something, they should donate it to a charity of my choice instead and not force me to pay for something I do not want.

Replies

By Brian -

Replies

By Brian - SAN DIEGO, CALIFORNIA -- In 9/2017 replaced car battery when car failed to start. Called AAA and tech arrived to my location in about 30 minutes. Tech tested battery and said battery needs replacing. Spent almost $190 with assurance the battery was warrantied for 3 years. Then on 9/1/2019 the battery didn't start. Gave it about 10 seconds, and the car started and was fine. I thought I should have it tested just in case, so a couple of days later, drove to Autozone to have battery tested to avoid using up a AAA service call. Autozone found the battery was very weak. I proceeded start car, and found the car was completely dead. Even the power doors wouldn't open.

So called AAA, they came out, tested and said battery was fine, yet car was dead. So another AAA came with flatbed and towed to my mechanic. My mechanic said the battery was dead and couldn't test the system to rule out. He checked wires and fuses, but found battery is dead and wouldn't hold a charge and recommended I have car checked at Chevy dealer. So called AAA for another tow to Jimmy Johnson Chevrolet. To check car out, it was going to cost $190. They tested battery found it was dead and tried jumping and still no start.

They said battery wasn't taking a charge, so they left charger on for 4 hours and by then AAA again came out and car finally started. AAA put their tester on and said battery was like new. So dealer said they would let car sit overnight and recheck. I get a call from dealer saying the battery seems to have a bad cell and that it might be 2 days or 2 months, but battery is going out. Yet AAA checks and says battery is like new and won't replace.

So after all this, I had to buy a battery from dealership as I think AAA tester is rigged to say it's ok even when battery has no power. So after all this, instead of just replacing my battery because of warranty, I had to purchase new battery. Final cost to me $322. Thanks to worthless AAA battery. So in short, 3 independent sources said the battery was bad and need replacing. AAA says the battery is like new so they won't honor warranty until battery is completely bad.

Replies

By LM - FARMINGTON, UTAH -- My recent experience with the AAA in Farmington Utah was lacking customer service, rather it was unacceptable. First off training needs improvement on policy and procedures, this needs to be consistent information. I received answers to questions that conflicted with each other (central call center vs a branch). I called the Farmington store phone number twice, both times to be rerouted to their central call center. Why I wasn't able to connect directly to the branch is beyond me. Why have a number if you aren't gong to answer it. I asked my questions, got the answers which I found out later were incorrect AFTER driving to the Farmington branch. I was told by Tiffani Cunningham that she couldn't take our pictures or print them (I had them digitally) because we are not AAA members. I will need to find someplace else to have them printed and come back.

Got the pictures printed and headed back to the Farmington branch for second time. I was then told I was still missing information. I asked Tiffani during the first visit what EXACTLY I needed to bring back with me. There was no mention of missing information/documents. By this point Tiffani was snarky and belligerent. From there Tiffani began arguing with me about whether or not she told me about the missing information. Do you really think I want to drive back to your office for a third time? Tiffani was not interested in listening to understand or offering customer service. She was wanting to be right. I asked if I could email the missing information/documents immediately, I had them in digital form. But Tiffani told me no, that I had to bring them in already printed. It was clearly apparent that she wanted to close the store and not help me. It was 5:45pm, they close at 6:00pm.

If any of my customer service employees treated my clients the way I was treated today by Tiffani Cunningham I would have immediately pulled them aside, had them apologize (whether right or wrong) and possibly let them go on the spot. For a company that is built on customer service, I am shocked that a Member Experience Generalist would treat a potential client in this manner. I can't help but think if they treat potential customers this poorly, I can only image how they treat their actual clients.

Replies

By No More AAA - ST PTERSBURG, FLORIDA -- I have been a member of AAA starting in 1980. They are NOT the same service company they were. At 1:30 one of my new tires had a blow out. They told me it would be 3.5 hours before they could send someone. After 4 hours a tow truck came. We did not get 5 miles when that tow truck broke down with my truck on it. I called AAA and they told me it would be at least another 3.5 hours for another tow truck. My story is about the same as the other ones on this site. What I did not read is why these long waits? I feel sorry for the tow truck drivers that have to deal with us. By the time they get there we are so upset. It is Not their fault but it is AAA fault. What is going on is AAA pays these companies so little that they don't have a lot of companies that will go under contract with them. This is what the driver shared with me. AAA pays them $25.00 for the hook up and after the first five miles $2.50 a mile. If they drive you 5 miles they only get the $25.00. They might of had to drive 15 miles to get to you, they don't get paid for that. It took about 20 minutes to get my truck on the tow truck. So by the time these tow truck drivers take that $25.00 and take out their time, gas, insurance and wear and tear there is no money left for them to feed their families. AAA should be ashamed of themselves. AAA is selling us their old reputation after taking our money they don't care about us or their drivers. They have to remember without those tow truck drivers there will be no AAA. Please remember not to take it out on the tow truck drivers but write a review. The ones that do come after 3-4 hours are over worked and under paid. I plan on looking for another company soon.

Replies

By John - PORTLAND, OREGON -- I've always believed AAA road side assistance was something you just had. I've been a member for more than 30 years.

I was driving home tonight, the gas light came on and said I had 50 miles to empty. I was about 4 miles from the gas station when the car sputtered and I coasted to the curb.

No problem, I have AAA. HA! What a joke. Now I know they sub contract the tow service. I appreciate the business model. I do expect they have a variety of suppliers and back up options. Apparently I gave them too much credit.

The guy who answered the phone was nice and pin pointed my location. Then wanted to sell me a AAA battery. I have a new battery and all of the electronics were working fine. Then he wanted to push a tow. I explained that I was fairly sure I needed gas, but yes, in the event that it wasn't the gas, I would indeed a tow. Finally he said the tow had been dispatched.

After about 40 minutes I received a call letting me know it would be at least 30 minutes more. Amazing how well they are trained to apologize. I finally had gas delivered on my own an I was off.

For the nearly $200 a year, once in 5 years I call and all I get is a polished apology . I was told they do the best they can. Well, tomorrow I cancel my AAA membership. A little research and I find a number of options, cheaper and some, including a service that came with the car - included.

When I called this morning to cancel my membership, they said, ok, thank you. Clearly my business isn't important to them. I now have AARP Roadside Assistance for less.

Replies

By PreciousMoments25 - TALLAHASSEE, FLORIDA -- I have been a AAA Member for over three years and this has been thus far the WORST CUSTOMER SERVICE EVER!!! I called to renew my membership because my car suddenly stop and would not crank. During the call the AAA Rep state that if I renewed my Premier membership I would have to wait 3 days before my car could be towed. She then suggested the Classic membership, this way I could get my car towed the same day without a waiting period and that I could add the Premier services at a later day since I would be already member without having to wait thee 3 day waiting period. I purchased the Classic membership as suggest and was able to get my vehicle towed that day. Almost a month later, I needed my car towed again, because I was given a notice to remove my car from the premises from the landlord because it was inoperable. So I called Stupid AAA and was advised that I would have to pay $138 extra because my Classic only covers 5 miles. Since I remember what the AAA Rep said from the previous tow, I decided to pay the additional cost $35 for the PLUS Membership. This Rep Zipporah then tells me I still have to wait 3 freaking days still and I would still be charged when the tow truck guy gets here. I was LIVID! I said this was not told to me when I renewed my membership. I was lead to believe that I wouldn't have to wait since I was already a AAA Member. "A BUNCH OF BOLOGNA . Then she puts me on hold for like 10 minutes, just to tell me that she can not assist me, before admitting to me that they did review the call that I had with the representative and that they can see how it was a miscommunication. Then she transferred me to Nathan who suppose to be a supervisor was a even more JERK and a Smart Mouth! AAA STAFF HAVE DEFINATELY DISPLAYED A DISSERVICE TO ALL CONSUMERS! PLEASE BEWARE!

Replies

By chadmurf269 - LENOIR CITY, TENNESSEE -- We arranged for AAA Septic Tank Service (Lenoir City) to come and pump our tank for $250. They arrived on time, and I informed them my gravel driveway was a little soft due to the weather we have had over the last few weeks. The driver attempted to drive up, but lost traction close to the top, digging 10 inch ruts for about 25 feet. He decided he couldn't make it up our driveway.

He wanted to look at the tank anyway, so we walked up to the house, where I had dug out the tank opening the evening before (to save us an additional $75). We opened the tank, and he poked around a bit, noting that, although the tank is nearly full...solid waste was caked around the entry. We poked the spot with a stick a couple times to knock it away (which might buy us another week) and replaced the cover. I told him I would let him know when the driveway (now with 10 inch ruts in it) was fixed and dried up enough for his truck. He said he might have to charge me a "service fee" but needed to call his boss to find out. (I thought maybe a small fee for driving out...no big deal. I know they have to pay for fuel and such).

About ten minutes later he told me his boss would require the service fee, which would be $150. So it cost me $150 for a messed up driveway and to poke a stick in my septic tank for 30 seconds. I pleaded with the company to be reasonable, but they would not budge on the fee. The tank will still have to be pumped, costing me the original $250, which will be with a different company.

I want everyone to know this in case the same situation occurs with them. Be aware that if AAA Septic says "I can't pump it but I'll take a look at it while I'm here" that they may charge you a very large fee. Ask them what it will cost for that "look" first. I don't know if all septic businesses would do this to you, just please be aware that this happened to us and we can't help but to feel like we were scammed. We will be out at least $400 when this is all over.

Replies

By Darlene - NASHVILLE, TENNESSEE -- The 2 times that I used AAA, I was disappointed. The first time I tried using them, I accidentally locked my keys in the trunk. They told me that it would be 45 minutes before anyone would show up. 1.5 hours later, nobody showed up. I called again. This time they told me that the guy got held up and they are not sure how much longer it would be. Finally, the guy who was supposed to show up called me and said it would be another hour before he got there and he does not know why AAA told him an hour. I was at a gas station where luckily a locksmith walked in and opened my trunk for me. I waited for over 2 hours and nobody ever showed up.

The second time I tried using AAA, I had a flat tire where I worked. Once again I was told it would be about an hour and once again after 1.5 hours I called again. The guy who was supposed to be there to help me with my flat informed me that he wasn't sure why they called him to come because he was located approx. an hour away in a completely different county. I don't understand why of all the tow truck business located in my big city, they called someone in another county. After the last incident, I let my service expire. I will just take my chances next time.

Replies

By spellunlimited - CALDWELL, NEW JERSEY -- I had terrible experience with AAA. First time when my car's tire got flat I called them and was told that the driver will be there in an hour. He didn't come until 2.5 hours of waiting. Luckily I was in the parking lot of my office. He finally arrived and did his job. Second experience was worst. There was an accident on a major highway and somehow the broken glass from that car got stuck in my car's tire eventually leading to a punctured tire. My car was sitting in the fast lane on a major highway with all the rush hour traffic coming in. I call AAA and told them to send someone quickly as I'm stuck in the fast lane of a highway.

They told me someone would be there in 20 mins. 40 minutes passed no one came. Finally a police officer came with a tow truck and moved me to the shoulder. The tow truck guy also changed my tire. The AAA guy never arrived. I was there for an hour and no one from the AAA company showed up. I called them again and told them that no one came and I no longer need them. Instead of being apologetic the representative told me that she cancelled my request so I don't get charged!

Unbelievable...charge for what??? I have been paying them all those years to help me when I need and they want to charge me extra? I would never ever trust AAA again. It is the worst insurance to have if you have an auto emergency.

Replies